What’s next for property investors after the ‘extraordinary’ election win?

Posted by APP Admin on 22 May, 2019 9:28 am

Last weekend’s federal election saw the Coalition government returning to power in an election that saw policy on property taxation a hotly debated topic. There’s plenty of discussion across all media sources this week.

We’ve summarised a couple here if you’d like a quick read for a property wrap up and what the next 12 months might look like for property markets around Australia.

The election is now over, and to the surprise of many, Scott Morrison will remain our Prime Minister.

So, how will the outcome of the federal election affect the value of your home and our property markets? Housing markets are likely to pick up by the end of the year.

The stability of government and the fact that there are not changes to negative gearing or Capital Gains Tax will encourage investors.

The market hates uncertainty, and the Coalition win should return confidence to our subdued property.

We began the year with two big stumbling blocks which have both been overcome.

1. The Haines Royal Commission into banking.

2. The Federal election

Now it’s time to get on with business as usual.

The timing of the bottom of this downturn will however depend upon the banks loosening lending restrictions and the timing of any interest rate cuts – the first of which seems likely next month and deliver a boost to our languishing markets.

Negative gearing changes off the table as Morrison holds government.

Mr Morrison holding power means the Labor Party’s plans to limit negative gearing to new housing from 1 January 2020 will not go ahead.

The same applies to Labor’s proposal to reduce the capital gains tax discount from assets held longer than 12 months from 50 per cent to 25 per cent, which will now not see the light of day.

What will go ahead under a Liberal government in terms of property policy is a boost for first home buyers, which Mr Morrison announced last weekend.

The Liberal government will allow first home buyers to purchase property with a 5 per cent deposit. This means some lenders will provide loans on a 95 per cent loan-to-value ratio.

The First Home Loan Deposit Scheme will be available through private lenders and small lenders, which Mr Morrison said is a bid to ensure competition on price for Australian borrowers.

Property investors should also keep an eye on where the billions promised in infrastructure spend is distributed, which may present growth opportunities in suburbs and regions which get a funding injection.

The Morrison government has announced $100 billion in infrastructure spend over the next 10 years, which is about $25 billion more than current levels.

Will property markets rally?

The jury is still out on how the markets will react to the Liberal victory, although it’s broadly accepted that prices will remain more steady under a Liberal government.

“The stability of a familiar government, and an expected interest rate cut in the coming months, will boost confidence in the property market and encourage vendors and buyers to reengage,” said LJ Hooker’s head of research, Mathew Tiller.

“Australian’s have been patiently waiting to see the outcome of the May 18 federal election before making a decision to act,” he said.

Labor’s proposed negative gearing changes were expected to rattle property investors, and soften values in capital cities in the short to medium term.

In addition, although modelling was mixed across the board, Labor’s negative gearing changes were also tipped to soften rental returns in capital cities.

New Wave of Southerners to Lift Property Prices – Courier Mail – Elizabeth Tilley

Posted by APP Admin on 1 April, 2019 9:55 am

The following is an article published in The Courier Mail Digital Edition on 16 March 2019, written by Elizabeth Tilley, Real Estate Reporter.

Queensland real estate is on the cusp of a boom fuelled by Sydney and Melbourne’s property woes, with a leading analyst predicting interstate migration to hit a record high by next year – putting upward pressure on home prices.

Research by Place Advisory , provided exclusively to The Courier-Mail , predicts gross interstate migration to the state could surge to more than 120,000 people by the end of June 2020.

That would surpass the level reached in 2002, which was a catalyst for double-digit house price growth.

The number of southerners flocking to the Sunshine State is at its highest level in 14 years – and it’s not just because of our warm weather and worldclass beaches.

Queensland recorded a gross interstate migration gain of 105,938 people in the 12 months to the end of last June, according to the latest Bureau of Statistics figures, with almost three-quarters coming from Sydney and Melbourne.

Last real price growth was in 2008

Place Advisory director Lachlan Walker said the last period of decent home price growth in Queensland was between 2002 and 2008 when interstate migration was high and the economy was soaring.

“We haven’t really seen real price growth since 2008,” he said.

“The floods in 2011 and 2013 really halted our marketplace, whereas the southern states have definitely seen significant capital growth.”

Mr Walker said that could be about to change, with growth in the range of around 7 per cent on the horizon.

“From now, we could start to see price growth for the first time since the last real cycle,” he said.

“We’re relatively affordable now compared to everywhere else on the eastern seaboard, and job opportunities are starting to arise, which should result in higher demand and higher prices. Realistically, we’re probably looking at 5, 6, 7 per cent (growth).

“Some years it could be higher, some years it could be slightly lower.”

Major infrastructure to inject $17 billion

According to the Real Estate Institute of Q u e e n s l a n d , major infrastructure projects are forecast to inject $17 billion into the Brisbane economy over the next six years.

“This sort of expenditure is boosting confidence, a key measure of market strengthening among most property industry stakeholders,” chief executive Antonia Mercorella said.

The REIQ cites tourism as one of the most promising growth industries.

Nerina Pratt (pictured) recently moved from Sydney to Brisbane for work and is renting in the city, but looking to buy a home in the near future.

She said she liked Brisbane’s “laid-back lifestyle” and affordability. “It’s definitely a change of pace,” she said. “I do think you can get more value for money here.”

Posted by Peter Spencer on 2 November, 2018 6:16 pm

We like property. We like it a lot. But it’s a big mistake to think property investing is a walk in the park and without risk. Investors can get burned in so many different ways. Many so-called advisors in the real estate property market don’t often talk about what could go wrong – the difficulty in getting tenants, dodgy tradesmen who have stuffed up your repairs, the stress of meeting your monthly financial obligations. Instead they present the highlight reel of huge rental returns, huge capital growth, and huge profits. Unfortunately, the truth about property investing is somewhere in the middle and a colourful mixture of The Good, The Bad and The Ugly.

Here’s our Top 10:

1). THE GOOD: Property is a reasonably easy asset to understand and get in to.

You can see it, touch it, walk around in it. You don’t need a 60-page prospectus to figure out what you are buying. Choose to either invest in a house, a unit, a commercial shop or factory, or a mixture of all. There are no complicated steps you need to take to get in to property. You organise your finance through a reputable Mortgage Broker who will source the best possible package and interest rate and help you get the paperwork in order to organise finance approval. Once you know what you can afford to buy, you’re on your way to finding the right property. This is where you might need to enlist the help of a property specialist. If you and your team thoroughly do your due diligence in terms of getting inspections and comparable valuations, there’s little risk of buying a lemon or overpaying.

2). THE BAD: You could pay more than you should.

If you do the selection process by yourself and, despite all your due diligence, you let emotion creep into your purchasing decision you could find yourself buying the fancy and way more expensive property. With its gourmet kitchen, spa bath and fireplace you can imagine yourself living in it, while not considering what the majority of tenants in Australia can afford. Your emotional betrayal has seen you pay more than you should have for the house, without the offset of being able to recoup a higher rental yield by a smaller number of potential tenants. Emotion in property investing is bad. To avoid the emotional wild card, get someone else to work with you in the selection stage to be your common-sense sensei.

3). THE UGLY: Maintenance can eat into your rental income.

Showers leak, dishwashers break, paint gets chipped, lights stop working. It is fair to say that the older the property the more repairs you’ll be up for as fixtures wear out and fittings break. Brand new properties will afford you a lovely buffer period of building and appliance warranties, but in time gutters will leak and carpets will need replacing. Be prepared to factor into your budget a percentage of your rent to cover repairs and maintenance.

4). THE GOOD: You have stability.

Real estate is less volatile than shares or mutual funds, especially is uncertain economic times. Even though “bubbles might burst” in some Australian markets, the continuing demand for housing fuelled by strong population growth ensures that property prices are supported. The real fear is a reduction in price. However, the price drop isn’t actually a reality until you decide to sell the property. If the property was purchased correctly and has been able to generate a healthy cash flow, the investment can be sustained until the price goes back up again.

5). THE BAD: It’s expensive to buy and sell properties.

To get in, it costs you a good whack for a deposit – a good start is 20% of the purchase price. Then there’s stamp duty, legal fees, property searches and valuations, and mortgage insurance if you don’t meet your lender’s comfort zone of 20% deposit. And then to get out you’ll have to pay an agent’s fee to sell your property, more legal fees and capital gains tax on any profit you make. One way to save a bunch of money is to build a house on a good block of vacant land. You’ll only pay stamp duty on the land purchase rather than on the total purchase price of an already-constructed home.

6). THE UGLY: Finding the right tenant might take longer than you want.

Vacancies are a fact of owning-investment-property life. Tenants come, and tenants will go. Even in the most in-demand and tightest rental markets you will occasionally experience an empty house. The best property in the best location is not immune to this unpleasant reality. As they say, timing is everything. For example, you do not want to be looking for tenants in the December/January period. Everyone is distracted, in transition, or worse, competitively looking for properties to settle in before the new school/work year. Get ahead of the game and time your leases to fall outside holiday periods and seasonal influences. A good property manager will help you understand the highs and lows in your market.

7). THE GOOD: Your Tenants and the Taxman will help pay off your investment.

Depending upon how much you have borrowed, your weekly rental income from your tenants will go a long way to meet your mortgage payments. And the interest you are charged, along with a whole slew of other expenses such as depreciation, property management fees, rates and repairs, all become tax deductions. This will considerably reduce your tax bill and improve your cash flow. A quantity surveyor will prepare a depreciation schedule. A good accountant can help you cut your tax expenses by thousands of dollars.

8). THE BAD: Tenants disproportionately have more rights than landlords.

Tenants have rights, and once you have tenants installed in your property it essentially becomes their home and not yours. You can’t make any changes to the property or even drop in for a casual inspection, without providing ample notice. And if something breaks on the property such as a dishwasher or microwave oven then you are obliged to replace it, if it formed part of the original leasing arrangement. Your property manager is your eyes and ears for the health and well-being of your investment property, so choose a good one. Regular inspections are a must – at least 3-4 each year – to keep on top of the overall condition of your property. There’s nothing worse than getting to the end of a lease to discover that your lovely house has been used and abused badly. Negotiating what is fair wear and tear and what is negligence from the tenants at the end of a lease can become a nightmare.

9). THE UGLY: Your property could get damaged, flooded, or catch fire.

Gotta love Australia’s extreme weather conditions. Firstly, don’t buy a property in a flood-prone area. Most local councils will have these areas zoned as such, so look elsewhere. And try to avoid dodgy tenants. Whilst every care is taken to screen potential tenants, sometimes you only discover the bad ones when it is too late, when they’ve left your property owing 4 weeks rent and walls that look like someone used them for batting practice. Fire, floods, storms, accidental damage and malicious damage are a fact of life and property investing. Plan for the worst and hope for the best. Get a good Landlord Insurance policy that will cover you for all contingencies, as well as loss of rent while making repairs after a major event.

10). THE GOOD: Property offers predictability and can make you rich.

Property is undoubtedly more predictable and makes more millionaires than any other asset class. With a well-chosen property you can look out to the future in 2 years and make a fair assessment on the direction the market pressures will be pushing, unlike the share markets where anything could change within seconds. Fortune Magazine has famously touted that 97% of all wealth was either created or held in property. But property is not a get rich quick scheme. Property investing is a long game, but a worthwhile one.

So there you have it. The trick with property investing is to ask the right questions of the right people and surround yourself with people that know more than you do. Listen to what makes sense, what seems non-sensical and what seems too good to be true.

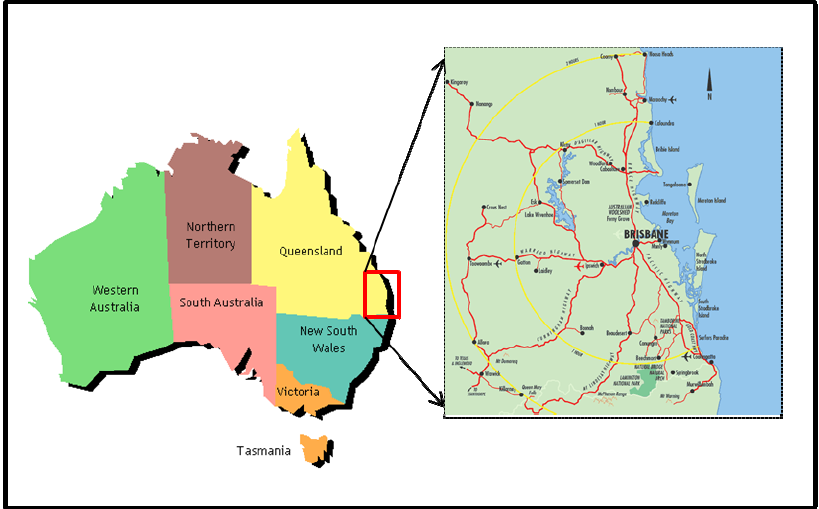

Brisbane and surrounds set to double in size by 2043

Posted by APP Admin on 10 October, 2018 2:58 pm

If you’re looking for property investment advice, you’ll be interested to know that a city almost twice the size of Brisbane will be added to Southeast Queensland’s population over the next 25 years. Just over 2 million more people will live here, swelling the number from 3.5 million to 5.5 million – more than currently living in the entire state.

According to leading demographer Bernard Salt, who has conducted exclusive research for the Courier Mail’s Future SEQ series, the Southeast Queensland of 2043 will be the same size as Sydney or Melbourne today. “It is quickly emerging as Australia’s third global force and, as such, it will offer all the urban amenity and quality you would expect from an urban conurbation of that scale.

“And yet it is quite unlike any other city in the country. Others are capital citycentric, like a fried egg with a big yolk in the centre and the white spreading outwards.

“Southeast Queensland is like the inside of a clock, with a big cog surrounded by several smaller cogs working together – the surrounding council areas in Greater Brisbane, The Gold and Sunshine Coasts and Toowoomba. They are independent but connected.”

Accommodating the additional people will require 794,000 extra homes by 2043.

What does that mean for you, a would-be property investor?

Well, if you’ve been wondering WHERE to purchase property, simple supply and demand would indicate that Southeast Queensland is the spot to be. What about the WHEN? Anytime from NOW will do. However, the sooner the better as land and house prices will only rise as demand begins to increase.

What will this new boom city look like?

Debbie Smith, the Brisbane managing partner of professional services firm PwC which conducted exclusive research and analysis for the series, says density would be the “defining characteristic” of SEQ 25 years from now. Ms Smith said, “In inner-city areas we expect to see super high-rise buildings functioning as mini cities and communities – no longer single-use buildings but vertical mixed-use developments incorporating any combination of uses from schools, retirement living, gyms, shops and commercial offices to residential apartments.

“Meanwhile, in our middle and outer ring suburbs we will see a push towards the creation of 30-minute neighbourhoods, where residents can access the majority of their needs within a 30-minute trip, be it walking, cycling or public transport.

“In our outer ring areas, we will see more upscaled master-planned communities to accommodate population growth.”

If you’re already sitting on property in Brisbane and surrounds, pat yourself on the back for a job well done. If you’re not, it’s not too late. The key is to start somewhere. Good property investment advice and assistance may be your best bet. Call or email us at APP for advice – it won’t cost you anything, just your time.

Posted by Andrew Jackson on 21 January, 2018 8:48 pm

Don’t get caught out by what you can’t see. Investing in sloping blocks of land that are located in hilly areas can often have a cheaper price point. On the surface, this might appear tempting, giving you more money to build with, but it’s what’s below the surface that could prove costly.

Sloping blocks in hilly subdivisions can often result in significant costs associated with long retaining walls, deeper footings and additional drainage and water management. Whilst necessary on these types of blocks, what these costs won’t return you is a higher rental amount from your tenant. So before you sign to purchase the bargain of the century, stand back, have a look at what the real cost of developing the block might be and think about whether an additional $30,000 spent on retaining walls and footings is money well spent.

Secure a better tenant and get your property rented sooner

Posted by Andrew Jackson on 2 September, 2017 9:20 am

So the suburb you’ve invested in now has five other properties for rent just as your property is being completed. They are all being advertised for the same rental amount and you run the risk of your property being vacant for 6 weeks until a suitable tenant is found. How can you get your property rented sooner?

If your property is worth $450 per week rent and it’s vacant for six weeks, it has essentially cost you $2,700 in lost rent. Here’s a couple of simple strategies to make sure this doesn’t happen to you:

Drop the rent by $20 per week and look to get it rented sooner. If the property rents straight away, on a six month lease it has cost you $520 but has got you a tenant sooner.

Offer a discount for paying in advance. This works particularly well for tenants who have their rent sponsored by their employers.

Look to value-add by offering a lawn-mowing and gardening service for the first six months. This will usually only cost around $20 per week, ensures the property grounds are well maintained and could very well become an arrangement your tenant wants to continue with (and pay for themselves) after the six months has ended.

Regardless of which option you choose, or if you have another option in mind, don’t simply be satisfied with joining the list of vacant properties. Work with your property manager to do something to make yours stand out from the crowd and get your property rented sooner.

1). Do you only look for properties in the NT? The short answer is no. The APP team look at property cycles around the country and have no single area, suburb, city or development. We actually look for sustainable growth.

2). Secondly I am asked about Strategies. This is a little more difficult to answer. What is your long-term strategy? Do you have one?

The first step you need to take if you are looking at setting a positive path for your future is to develop a strategy. Or you can use the one that has been developed by APP. You need to trust in your strategy, and stick to it. Property is long term; we purchase and hold. If you find the right property, would you sell it or watch it grow?

Success requires many things. You need to be informed and have a solid understanding of what you are doing, but equally important is the need to be disciplined and patient. If you want to understand our process and how it can be duplicated to work for you, come to a workshop or give me a call to have a chat.

But ask yourself: Do I have a strategy? What is my strategy? After all, it is your future.

Share on Facebook

What will the 2017 Budget mean to me, an Investor?

Posted by Peter Spencer on 16 May, 2017 11:43 am

I want to be a Property Investor. What will the 2017 Budget mean to me?

That’s an excellent question.

The following is a brief summary of what the main points are that may affect current and would-be Australian Resident Property Investors—keeping in mind that at this stage these are only proposals that will have to be passed by both the House of Representatives and the Senate, of which the government does not hold a majority.

What’s NOT affected:

Any existing investment properties purchased, ie. contract exchange date, prior to 9 May 2017 is not affected. Nor are commercial, industrial and other non-residential properties.

Negative gearing isn’t tabled to change, nor has the Capital Gains Tax 50% discount. (This is proposed to actually increase to 60% if you elect to invest in qualifying affordable housing).

Capital Works deductions, ie. depreciation of your building over 40 years, has not been affected. This deduction in itself has always been a great reason why you would choose to purchase a brand new property as an investment, especially a new build, as you get the maximum benefits each and every year, for 40 of them.

It might change, but it’s not all bad news:

Probably the biggie here is that Plant and Equipment depreciation deductions will be limited to new purchases only. Therefore, if you purchase a property that is NOT new the existing plant and equipment will be reflected in the cost base for capital gains tax, rather than deductible each tax year. To gain the best tax deductions you would be best to purchase a brand new build and as the first owner, enjoy full depreciation of all plant and equipment. You will need a Quantity Surveyor’s report to make your claims.

Existing property investors may consider it prudent to hang on to their current properties to continue claiming depreciation on the plant and equipment, as their next investment may not enjoy the same deductions if they purchase a less than new property. Brand new properties will always provide the best tax deductions, especially if this new budget is passed.

Travel Expenses to inspect, maintain and collect rent will no longer be deductible for properties held interstate. Property Management fees are still fully tax deductible, so ensure you engage one to do the work for you.

First Home Buyers can make voluntary contributions into their superannuation up to $15,000 a year, and capped at $30,000 in total. These contributions, plus earnings can then be drawn down to use as a deposit on their first home. Think of it as a super-charged savings account.

In addition, First Home Buyers can still take advantage of the First Home Buyers Grant, which can be used to purchase your first investment property instead of your first principal place of residence. So you can invest first if you wish.

As mentioned already, these are only proposals at this stage, so watch this space if/when it becomes real.

Share on Facebook

Investing: It’s all in the numbers…

Posted by Andrew Jackson on 2 May, 2017 10:04 am

Some clients can be funny with numbers.

I have a friend who won’t drive a car if the number plate adds up to 13, while another refused a block of land because it didn’t have an 8 in the lot number.

Superstitions aside, the real numbers investors should be concerned with are far more important. Here’s just a few to be thinking about.

The amount of weeks that your property is rented per year. The more weeks your property is rented the better the rental yield. Vacant properties only cost you money so lease it as quickly as possible.

Six-monthly or twelve-monthly leases. Every time your lease renews, your property manager is likely to charge a lease renewal fee, so twelve-monthly leases will essentially halve this cost.

A depreciation schedule, completed by a qualified quantity surveyor, could be the best money you’ll ever spend on your investment property. It will usually provide you with some big numbers to apply to your tax return for every year you hold your investment property, especially if it’s a newly built one.

Every two years, sit down with your mortgage broker and ask them to do two things for you. Firstly, review the valuation of your property to consider what equity has been built during this time, and secondly to review the interest rate you are paying on your investment loan. The combination of equity growth and a reduction in your interest rate could very well provide you with an option to reinvest into another property.

Share on Facebook.

Depreciation: how will you benefit at tax time?

Posted by Peter Spencer on 21 February, 2017 2:05 pm

The tax benefit most investors miss out on.

Everyone knows that one of the key ways to maximise investment returns is to be smart about your tax. Getting the most out of your deductions can be the difference between so-so returns and reaching the lifestyle you want. So why do so many people miss out on a fantastic source of deductions? It’s not interest on your mortgage and it’s not maintenance or repairs. In fact, it’s so intangible that you won’t see it unless you know it’s there. We’re talking about depreciation; the loss of value of your items.

A simple analogy that most people will be familiar with is the purchasing of a new car. Whatever the price you pay at a dealer, once it leaves the driveway you know its value has decreased. Suddenly, it’s a second-hand car and you can’t sell it for the same price you just paid for it. The same goes for a new house, fittings and fixtures. The difference is that if you’re using these items as a source of income, then you can claim this loss of value against your tax liability. So why do so many people miss out on this? The simple answer is they’re just not aware it exists.

Get the right advice.

To understand your entitlements, you need to draw up a tax depreciation schedule. This outlines what items are depreciating in value and at what rate, in line with the appropriate tax rules and regulations. If this all sounds like unfamiliar territory, then it’s recommended that you engage a registered Quantity Surveyor. As one of only a few professions recognised by the Australian Tax Office to have the appropriate skills to estimate construction and building costs for depreciation, you can be assured they’ll get the most accurate record of your entitlements. This one-off cost of as little as $400 can provide ongoing savings that far outweigh your initial outlay.

The depreciation schedule should include the following items;

A detailed forty year forecast table illustrating all depreciable plant and equipment items together with the capital works deductions.

The difference in claims using both the prime cost and diminishing value methods of depreciation.

A comparative table of the two methods of depreciation.

In a similar vein, you should ensure that your accountant is familiar with property investment. The correct accountant can assist you to set-up tax effective financial structures, allowing you to reach your investment and lifestyle goals faster. An accountant with a real passion for property is a great sign that they’ll be able to get the most out of your investment.

Now is the time to act.

Don’t leave it another year and miss out on deductions that can help boost your portfolio. Set yourself up for next year’s tax time now, and get yourself a tax depreciation schedule. If you want any more information, then come and see us at Australian Property Panel. We believe that having the right team behind you makes all the difference in the world. That’s why we make it out job to not only provide you the information you need, but to link you with the right people to see that your investments work for you, bringing you closer to the lifestyle that you desire.